There is a specific trap that only shows up when things go well, which makes it harder to notice than almost any other trading mistake. A trade wins, the account balance goes up, and the natural response is to feel like something was done right. Sometimes that feeling is accurate. Sometimes it is completely disconnected from what actually happened, and the win is masking a decision that had no business working out the way it did.

This is outcome bias, and it is worth taking seriously because of how quietly it operates. A bad entry that loses money gets scrutinized. Nobody defends a losing trade taken on a hunch. But a bad entry that happens to win rarely gets the same scrutiny, because the result feels like proof the decision was sound. It was not proof of anything except that, on this particular occasion, the market moved in a direction that rescued a flawed decision before the flaw could cost anything.

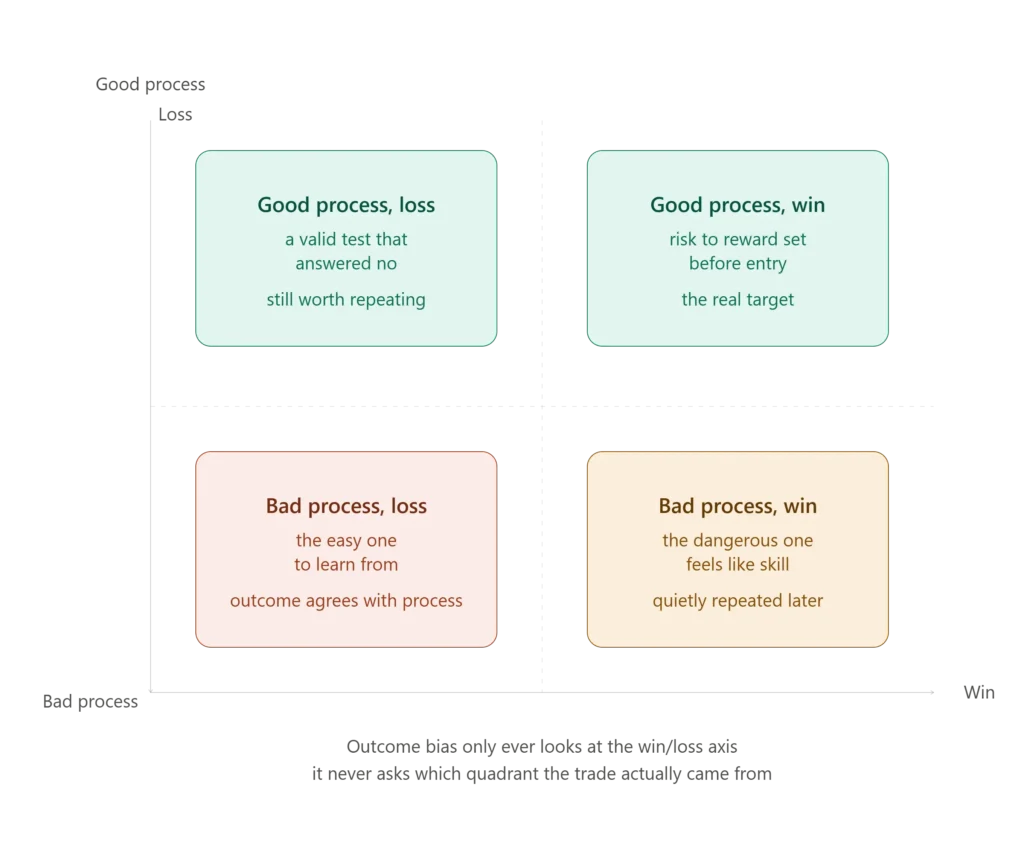

Why outcome and process are actually two separate questions

It helps to treat every trade as having two completely independent things worth evaluating. One is the outcome, did it make money or lose money. The other is the process, was the decision to take the trade actually sound given what was known at the time it was made. These two things are correlated, especially over a large number of trades, but they are not the same question, and treating them as the same question is exactly what outcome bias does.

A good process does not guarantee a winning trade. Markets are genuinely uncertain, and even a well reasoned entry with a favorable risk to reward can simply not work out, for reasons that have nothing to do with a flaw in the decision. A bad process does not guarantee a losing trade either. A stock can move in your favor despite an entry that never should have qualified under your own rules, purely because the broader trend or a favorable news event carried it there anyway.

The problem is that only one of these two questions is visible without effort. The outcome is right there, in your account balance, immediately obvious. The quality of the process requires actually going back and asking honest questions about what you knew and what you were risking at the moment you decided, which takes real effort and a willingness to be critical of a trade that technically worked.

Why a winning trade with a poor risk to reward is still worth flagging

Consider a trade where the actual risk to reward, calculated honestly using the real stop loss level and a realistic target, comes out close to even, roughly one to one, well below whatever minimum standard you have set for yourself. If that trade wins, it is tempting to file it away as a clean success. But the ratio itself did not change because the trade won. You were still risking close to as much as you stood to gain, and that is a losing proposition if repeated enough times, regardless of what happened on this specific occasion.

This is worth sitting with directly, because the instinct to celebrate a win and move on is strong, and it actively works against learning anything useful from the trade. If a similar setup shows up again next month, with the same underlying risk to reward problem, the version of you that only remembers this trade winning is more likely to take it again, carrying forward a flawed standard because the last example of it happened to work.

Why a losing trade with a good process deserves a different reaction than a losing trade with a bad one

The flip side matters just as much. Not every loss is evidence of a mistake. Some losses come from a properly reasoned trade that simply did not work, the market genuinely surprising a decision that was sound given the information available. If you had a real edge, a defined entry trigger, a sensible stop, a favorable risk to reward, and the trade still lost, that is meaningfully different from a loss caused by ignoring your own rules, chasing an unconfirmed setup, or placing a stop with no relationship to actual price structure.

Treating both kinds of losses the same way, as failures to be avoided in the future, risks teaching the wrong lesson. A well reasoned trade that lost does not need a different process next time. It needs to be repeated, because a sound process that loses occasionally is not broken, it is just operating in a genuinely uncertain environment. Confusing this with a process failure can lead to abandoning a good approach purely because it did not work on one specific occasion, which is its own kind of costly mistake, just less discussed than chasing a bad setup.

Why this bias specifically punishes self examination

I think the reason outcome bias is so persistent is that it actively discourages the exact behavior that would normally catch it, going back and questioning a trade that made money. There is very little internal pressure to review a winning trade critically. It feels finished, resolved, successful. The natural instinct is to move on to the next decision rather than dig into whether the win was actually earned by the process or simply delivered by the market despite the process.

This creates an asymmetry in how a trader’s actual skill develops over time. Losses tend to get reviewed, sometimes obsessively, because the discomfort of losing money creates real pressure to understand what went wrong. Wins, especially clean, satisfying wins, rarely receive the same treatment, which means an entire category of decisions, the ones that worked despite being flawed, tends to go completely unexamined. Over enough trades, that gap becomes a real cost, because those flawed but rescued decisions are exactly the ones most likely to be repeated without correction.

A simple habit that counters this directly

The fix here does not require a complicated system. It requires asking one honest question after every winning trade, not just the losing ones. Would I have taken this exact trade, with this exact entry and this exact risk to reward, if I had known in advance it was going to lose. If the honest answer is no, that the trade only looks reasonable in hindsight because it happened to work, that is worth writing down with the same seriousness as a losing trade’s post mortem.

This question works because it strips the actual outcome out of the evaluation entirely and forces a judgment based purely on what was knowable and calculable before the trade played out. A trade with a genuinely sound process passes this test regardless of outcome, because the reasoning holds up independent of what actually happened. A trade that only looks good because it worked fails this test immediately, and that failure is the useful signal, not the profit that technically resulted from it.

Why this matters more the longer you trade

The cost of outcome bias compounds specifically because it is invisible in the short term. A single flawed trade that happened to win costs nothing in the moment, and might even feel like validation. The actual cost shows up later, across dozens of similar decisions made with the same underlying flaw, some of which will not get rescued by the market the way the first one did. By the time that cost becomes visible, it is usually spread across enough trades that it is hard to trace back to the original habit, an early winning trade that never got questioned simply because it worked.

Reviewing wins with the same honesty applied to losses is not a natural instinct, and it will not feel necessary in the moment a trade closes in your favor. But the trades most worth examining critically are often exactly the ones that feel like they need no examination at all, precisely because they ended well. A result you are satisfied with is not the same thing as a decision that was actually correct, and learning to tell those two things apart, trade by trade, is what eventually separates a process that holds up over hundreds of decisions from one that only looks sound in hindsight, one lucky win at a time.