This is the twenty-fifth post in my Real Trade Series, where I go through actual trades from my own charts and journal notes, wins, losses, and everything in between. Most of the trades in this series come with some kind of note attached, a reason I wrote down at the time, a doubt I flagged, something that lets me reconstruct my own thinking months later. This one doesn’t. I have the entry, the stop, the exit, and the dates, and nothing else. I think that’s worth publishing too, because it’s honest about a real gap in my own record-keeping, not just a gap in my trading process.

A general note that applies to this post and several others in this series: the open and close dates and times shown come from when the trade was recorded in my trade journal, not necessarily the exact timing the order was actually placed and filled in the market. There can be a gap between the two, and readers should discount the precise timestamps accordingly rather than treating them as a live, tick-by-tick record of execution.

A quick note on the chart, if one accompanies this post: I wouldn’t have a saved screenshot from the actual dates of this trade, so any markup would need to be done on today’s chart, with the entry and exit placed at the historical prices and dates pulled from my trade journal.

What the record actually shows

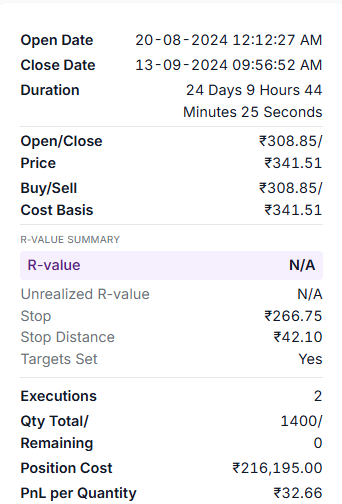

I opened a position in Kopran on 20th August 2024 at 308.85. My stop was set at 266.75, a risk of 42.10 per share, which works out to just over 13.5% below my entry price. That’s a wider stop than most of the other trades I’ve written about in this series. EPL had a stop roughly 12.4% below entry. HONAUT was tighter still, around 6.5%. A stop this wide on Kopran tells me something about the trade even without a note explaining it, either the setup itself required more room to work because of how the stock typically moves, or I was less precise about where I placed the stop than I usually am.

There’s no profit target logged for this trade at all. Every other position I’ve written about in this series had a target set before entry, even the ones that didn’t reach it. Its absence here isn’t necessarily a red flag on its own, but it is a gap, and I’d rather note the gap than pretend it isn’t there.

What actually happened

I held the position for just over 24 days, closing it on 13th September 2024 at 341.51. That’s a gain of 32.66 per share, which against a risk of 42.10 works out to roughly 0.78R, just under three quarters of what I was risking to make the trade. The net result was a gain of 22,112 rupees after costs, a real and meaningful win in absolute terms, even if the R-multiple itself is more modest than the headline number suggests.

Twenty-four days is a fairly typical hold for the kind of weekly breakout setups I trade, similar in length to Kopran’s own timeline and not far off HONAUT’s six-day sprint scaled up, or GHCL’s 24-day drift that went the other direction entirely. The difference between Kopran and GHCL is instructive on its own. Both trades ran almost exactly the same duration, 24 days for Kopran against roughly 24 days for GHCL as well. One ended in a genuine gain of just under 0.8R. The other ended in a small loss, not because a stop got hit, but because the stock went nowhere for over three weeks before I closed it out slightly under my entry price.

That comparison matters more than it might seem at first. Duration alone tells you almost nothing about whether a trade is working. Two positions can sit open for the exact same stretch of calendar time and produce completely opposite outcomes, and the number of days held explains none of that difference. What actually separates a Kopran from a GHCL isn’t how long either trade lasted. It’s the price action inside that window, whether the stock is actually trending in the direction of the trade or simply chopping sideways while capital sits tied up waiting for a decision one way or the other. I don’t have the day-by-day detail on Kopran to say precisely what that price action looked like along the way, only the entry, the exit, and the fact that the net result was positive. That’s a real limitation in what I can honestly say about why this trade worked.

There’s one more detail worth being honest about here. Looking at the chart now, my exit on 13th September landed close to the top of the entire move. Within weeks, Kopran rolled over hard, dropping sharply through October and continuing to bleed lower well into 2025, eventually giving back more than half its value from where I closed the trade before it finally found a base again. Without a note explaining why I exited when I did, I genuinely can’t tell you whether that timing was a deliberate, well-reasoned decision or simple luck. It’s entirely possible I got out because I’d hit some internal comfort level with the gain, and the fact that the stock then collapsed right afterward had nothing to do with my reasoning at the time. I’d rather say that plainly than let a good outcome imply a good process I can’t actually verify.

It’s also worth comparing the R-multiple here against some of the other wins in this series. HONAUT closed at just over 3R. CYIENT came in around 1.1R. EPL landed near 0.5R. Kopran, at 0.78R, sits roughly in the middle of that range, a solid outcome without being an exceptional one. If I had to guess, without a note to actually confirm it, the wider stop on this trade likely capped how favorable the risk-reward could look even with a healthy absolute gain, since a bigger denominator in the R calculation means the same rupee gain translates into a smaller multiple than it would on a tighter, more disciplined stop.

Why I’m publishing a trade I can’t fully explain

It would be easy to skip this one. It’s a win, the number is respectable, and there’s no obvious lesson sitting in a note the way there is with CYIENT’s missed EMA check or EPL’s unanswered entry-timing question. But I think that instinct, to only write up the trades with a tidy explanation attached, is itself a kind of dishonesty. If I only ever publish the trades where I can point to exactly what I was thinking, I’m quietly implying that every trade I take comes with that level of clarity. This one doesn’t, and pretending otherwise would undersell how much of real trading happens without a perfectly annotated thought process behind every decision.

The wider stop and the missing profit target are the two most honest things I can say about this trade. A 13.5% stop is a real commitment of capital risk, wider than I’d want to justify without a specific reason, and I don’t have that reason on record. It’s possible Kopran’s typical volatility genuinely warranted a stop that wide. It’s also possible I was simply less disciplined about entry precision on this one than usual, and a wider stop is often what happens when the entry itself isn’t as tightly defined as it should be.

What this trade taught me, even without a note to lean on

The lesson here isn’t really about Kopran’s chart pattern or the eventual result. It’s about the gap in my own record. Every trade in my journal should have enough written down at the time, even a single line, that I can reconstruct my reasoning months or years later without having to guess. This trade is a reminder that I don’t always do that consistently, and a win doesn’t excuse the gap. If anything, a profitable trade with no note is more dangerous than a losing one, because there’s no natural prompt to go back and ask what went wrong. The outcome was fine, so the missing process is easy to overlook.

Going forward, the actual takeaway from Kopran isn’t a chart lesson. It’s a journaling one. A stop this wide, and a target that was never set, both deserved a sentence of explanation at the time, and neither got one. That’s on me, not on the market, and it’s worth admitting plainly rather than dressing this trade up with a lesson I’d have to invent after the fact just to make the post feel complete.

There’s a broader point buried in publishing a trade like this alongside the ones that come with fuller explanations. A trading record that only ever shows the well-documented decisions is a curated one, whether that curation is intentional or just a byproduct of which trades happened to get notes attached at the time. Real trading includes positions like this one, profitable, unremarkable in their process, and genuinely hard to learn much from beyond the fact that the underlying discipline of writing things down slipped on this particular day. I’d rather this series include a few trades like that than only ever show the ones where hindsight makes the lesson obvious.